The destruction of seemingly safe, cashlike assets -- and the resulting surge in the liquidity premium -- is the other part of the story. The past few decades have been marked by the rise of the so-called shadow banking system: securitization largely replaced traditional lending, while investors clamored to maximize returns on the putatively safe (but uninsured) holdings the unregulated system created. This was the great irony of the post-tech bubble economy: the juxtaposition of brazen, unhinged risk-taking among lenders with the extreme risk-aversion of investors. The financial alchemy of securitization and tranching (and sometimes re-tranching) reconciled -- indeed, facilitated -- these divergent aims for a time, before reality intruded.

Here is Steve Randy Waldman's incisive description of this dynamic:

[There was] a “giant pool of money”, specifically sovereign and institutional money, that was seeking out ultra-safe, “Triple A” investment, and sometimes agitating for yield within that category.... The investors in question weren’t, in fact, investors at all in an informational sense. To a first approximation, they paid no attention at all to the real projects in which they were investing. They were simply trying to put money in the bank, and competitively shopping for good rates on investments they could defend as broadly equivalent to a savings account.What type of assets made up these quasi-savings accounts? Chief among them were AAA mortgage bonds, auction rate securities, commercial paper, and repo. Money-market funds that invested in these assets let retail investors get in the game too. The obvious appeal of these assets was that they were supposed to be as safe and as liquid as the cashlike assets that exist under the aegis of the regulated financial system -- i.e., T-bills and checking deposits (at least up to the FDIC-insured limit) -- while offering more yield. Unfortunately, this was a fantasy.

Losses and illiquidity migrated up the proverbial food chain of cashlike assets due to financial linkages and panic. This was an old-fashioned, albeit slow-motion, bank run on our modern financial system. The implosion of the AAA mortgage bond market first turned auction rate securities illiquid, as investors scrambled to sell the latter to make up for losses on the former. There were no buyers. The exposure of the banking system to its own subprime CDO dreck was the next accelerator. Worries about Lehman Brothers' solvency due to its toxic mortgage portfolio ultimately caused its funding in the repo market to evaporate -- and with it, nearly the remainder of cashlike assets in the economy.

Money-market funds were the next casualty. A few days after Lehman's bankruptcy, the Reserve Primary fund infamously "broke the buck" due to its holdings of short-term Lehman debt. A run ensued on money-market funds. Only a temporary government guarantee quelled the panic. The commercial paper market seized up next. This time, the Fed stepped in to lend directly to corporations. The ultimate fear -- that depositors might start a 1930s-style run on bank accounts above the $100,000 FDIC-limit -- led to accounts being insured up to $250,000 instead.

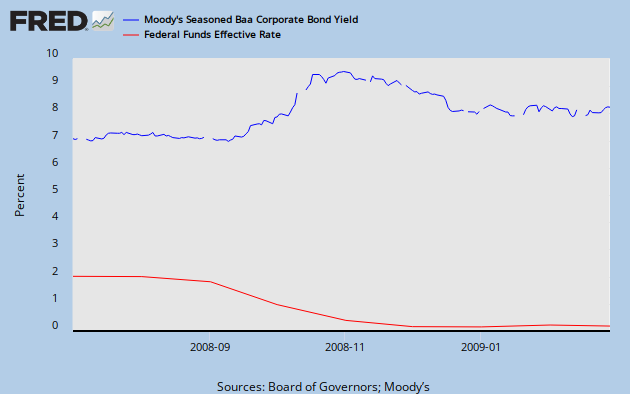

This wholesale demolition of cashlike assets naturally sent the premium for any remaining such assets through the roof -- or, in the case of Treasuries, to negative yields. This had disastrous implications. As Matt Rognlie points out, when the Fed Funds rate hits zero, the liquidity premium replaces T-bills as the effective benchmark for every interest rate in the economy. Hence, the yields on corporate bonds rose to ruinous levels in late 2008 despite the Fed's efforts to ease policy. The abyss beckoned.

{kind=link}

Thankfully, policymakers managed to arrest the collapse. Capital injections into the banking system ended the run on cashlike assets. The Fed's credit easing program, i.e., QE1, pushed the liquidity premium down to normal levels by trading cash for illiquid assets like mortgage bonds. And the much-maligned ARRA not only put people to work and money in their pockets, but financing it also necessitated creating new cashlike assets: more T-bills. Recovery, however, remains elusive. The civilian employment-population ratio has not shown any sustained improvement since the recession technically ended in June 2009. Our economic hole is as deep as ever.

{kind=link}

Could it happen again? In the short-term, it's difficult to see how another run on cashlike assets could develop given that the securitization machine is still idle. Treasuries are now essentially the only destination for investors to park their piles of cash -- which explains why yields continue to push down to historic lows. Of course, in the long-term, another panic in the shadow banking system is too possible considering that its basic financial architecture remains unchanged.

The rise of the "giant pool of money" has overwhelmed our financial system. Consider that in 1990 these piles of cash held by corporations and asset managers amounted to just $100 billion; today that sum has multiplied to $2-4 trillion. Any story purporting to explain why this has occurred certainly involves a fair amount of hand-waving. Some of the usual suspects include the move towards defined contribution pension plans; globalization and the subsequent decreasing share of revenue going to labor; the liberalization of markets as the Iron Curtain came down; and the centralization of financial institutions (note this does not even include the neo-mercantalist policies of the China bloc recycling their trade surpluses into dollar-assets). These gargantuan sums were simply too big for our insured financial system. Even with the recent move by the FDIC to permanently lift its limit to $250,000, only 33% of this money is held in deposit.

Deregulation and a stance of malign neglect allowed the shadow banking system to develop a seemingly safe place for these vast sums. Now that the illusion of liquidity has been broken, it is clear that right now the government must run mega-deficits to replenish the supply of safe financial assets for the private sector, and that some kind of reform is necessary to make our unregulated financial system safer.

As policymakers responded to the banking crises of the 1930s with deposit insurance, so must we too respond to our shadow banking crisis with some equivalent of the FDIC.

No comments:

Post a Comment