There are still two vacant seats on the Federal Reserve Board. The governing structure of the Fed is a bit abstruse, but what this means is that Bernanke has two fewer allies on the FOMC -- which votes to set monetary policy -- than would normally be the case. Maddeningly, Senator Richard Shelby (R-Ala.) has blocked President Obama's efforts to fill the empty seats on the Federal Reserve Board -- with the laughable excuse that Obama nominee and recent Nobel prize winner Peter Diamond is not enough of an expert in monetary policy.

It's not clear how much of Shelby's obstructionism is payback for the Democrats blocking conservative favorite Randy Kroszner's appointment to the FOMC during the Bush years, and how much is a matter of ideology. Nor is it clear if anybody would be acceptable to Shelby today. Indeed, part of Shelby's stated opposition to Diamond came from the latter's public support of QE2 -- which Mike Konczal points out would rule out Shelby voting for even Kroszner today. Already, one of Obama's two most recent appointees has dropped from consideration. It seems unlikely the spots will be filled in the near future.

Why does this matter?

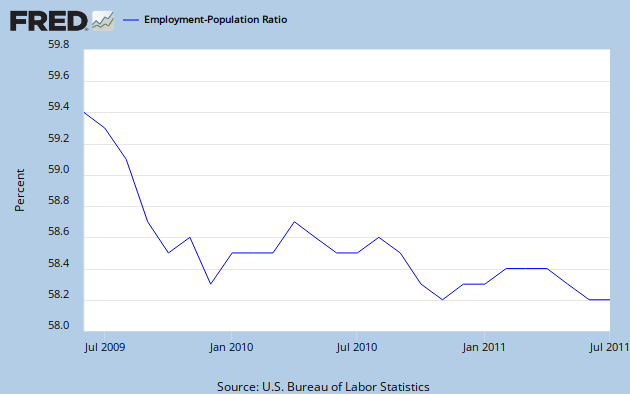

The FOMC usually tries to reach a consensus in its policy decisions. Its last meeting was an outlier, with three dissenters opposing the mild change in communications that the Fed expects economic conditions to warrant keeping short-term rates at zero through mid-2013. Unfortunately, these dissenters subscribe to what I like to call Don Quixote economics: waging war against imaginary problems while actual ones persist. Indeed, with the ten-year implied inflation at just 2% -- and falling -- worries about potential stagflation are profoundly misguided, particularly given that the civilian employment-population ratio is worsening. This bloc of self-styled inflation hawks have succeeded in stymieing more expansionary policy, only relenting when inflation expectations fall below the Fed's tacit 2% target -- which, thankfully, averts complete collapse, but regrettably does little to promote robust recovery.

{kind=link}

Two more dovish votes on the FOMC would obviously give Bernanke more latitude to push for unconventional policies, without having to worry as much about losing a vote to the inflation hawk camp. And clearly, the case for further monetary easing is made more urgent by Congressional Republicans not only blocking further fiscal stimulus, but also actually pushing for mild austerity.

Of course, Obama could end this confirmation charade, if he wanted to. Indeed, I just want to say two words to the president, just two words: recess appointments. Senate Republicans have, predictably, attempted to prevent Obama from even going this route by holding pro forma sessions every three days during their recess, but as Think Progress points out, this is a legally dubious tactic. In a similar case in 2004, the Eleventh Circuit court ruled that there is no minimum time Congress must be out of session before the President can use a recess appointment. So why isn't Obama filling the vacancies on the Fed that urgently need to be filled?

There are no good reasons. The most plausible is that Obama is wary of appearing too partisan and damaging his brand as the most reasonable person inside the Beltway. This is a mistake. The only issue voters know less about than the FOMC itself is how its members are appointed. Republicans might score a few political points on Obama's "overreach" for a news cycle or two, but 14 months from now that will be irrelevant. What will be relevant is the state of the economy -- and with fiscal policy on the sidelines, the Fed is the last, best chance of generating faster growth.

Obama's re-election chances could very well hinge on whether he gets religion on monetary policy. Does anybody in the White House realize this?